March 2026 Property Market Update: War, Rates & What It Means for Australian Borrowers

It’s been a tough month. A conflict thousands of kilometres away is being felt much closer to home, at the petrol pump (perhaps less so if you’ve got an electric car), in the supermarket, and in mortgage repayments. We know many of you are doing the sums at the moment and feeling the pressure, and that’s completely understandable.

A War That Hits Home

Disruptions to global energy supply have pushed oil above US$100 a barrel, driving petrol prices sharply higher across Australia. And it’s not just fuel. Higher energy costs are now flowing through to transport, goods, and services, when they were already high as we showed last month, adding to what was already an expensive economy.

Rates Moving Higher Again

Against that inflationary backdrop, the Reserve Bank of Australia (RBA) has moved again, lifting the cash rate to 4.10 per cent. Importantly, the latest inflation data doesn’t yet reflect these rising energy costs. As they begin to flow through, inflation data is expected to increase, which is why money markets are now pricing in the potential for further rate rises. See here what the money markets are saying our cash rate will get to. Many of the big bank economists agree with the money markets, in that we are likely to get more cash rate rises this year.

This yield curve is saying that in 3 years, the markets forecast our cash rate to be circa 3 rate hikes higher, than where it is now.

What This Means for Your Loan

For borrowers, the impact of rate hikes is pretty much immediate. Most major banks have passed on the latest increase to our cash rate in full. For a $750,000 loan, that’s roughly $118 more per month, and around $235 more since the start of the year.

When combined with higher costs across fuel, groceries and insurance, it all adds up and when economists from all the major banks expect to see more hikes, it’s not easy to swallow as a borrower.

Fixed Rates Have Moved Higher

At the same time, fixed rates have continued to rise, with most popular 2 or 3 year fixed rate loans now sitting above 6 per cent. This increase is being driven by increases in wholesale funding costs, which is what you see above. As a result, we’re seeing more clients revisit their residential lending structures, considering whether splitting their loan between fixed and variable could provide a balance of certainty and flexibility.

It’s not the right approach for everyone, but in a changing environment, it’s a strategy that requires important consideration given the current times. We wrote about the importance of considering a fixed rate in last month’s update, just before the war began and it’s still, a strategy that should be considered by all when it comes to hedging themselves against future rate rises.

Property: Holding, But Shifting

Despite the uncertainty, the property market has remained relatively resilient, though the dynamics are changing.

Recent insights from Cotality highlight a shift in behaviour. When rates rise, borrowing capacities tighten. When you add the expectation that rates are going to go higher, there’s no surprise to see buyer demand soften.

At the same time, lower-priced segments of the market are continuing to outperform, given the state and federal government initiatives underpinning these markets.

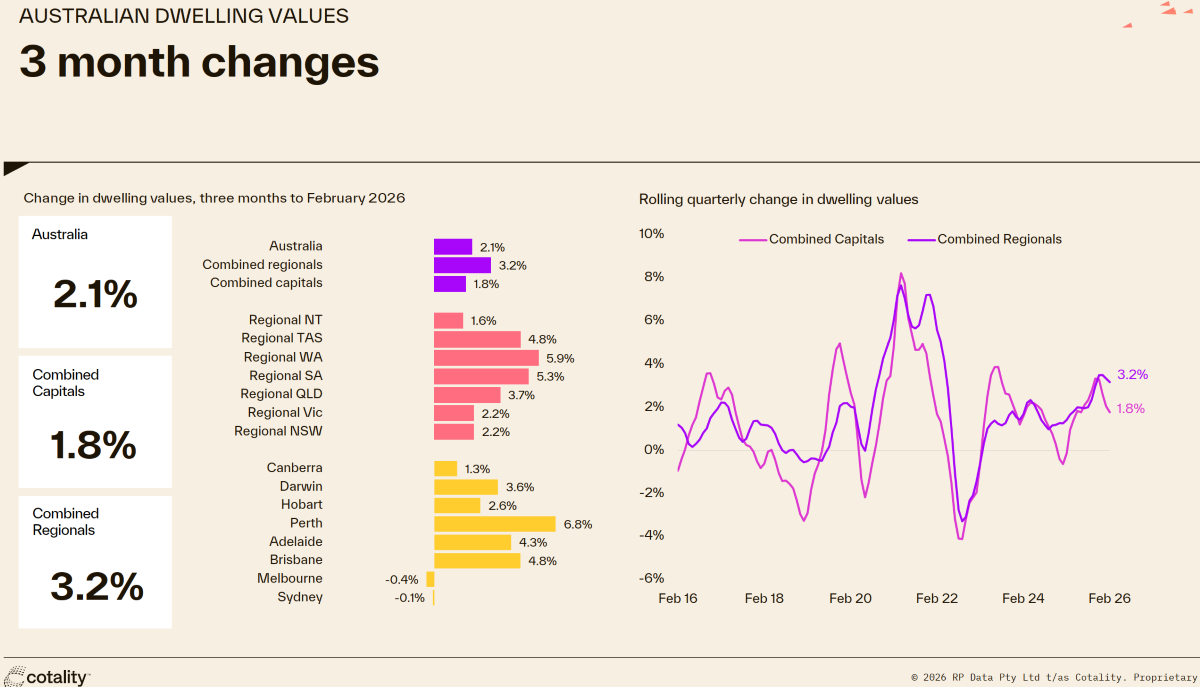

On a state-wide basis, Cotality’s 3 month changes in property data show Perth, Brisbane and Adelaide continuing to hold strong, supported by population growth and limited supply. Sydney and Melbourne, on the other hand, are feeling the impact of higher rates more noticeably.

Confidence Is Low, Creating Opportunities

Consumer confidence has fallen sharply. Fewer buyers are active. Auctions are becoming more subdued. Decisions are taking longer. But it’s also worth recognising what this creates.

When confidence is low, competition tends to ease. And for those who are well-prepared and have their finances in place, it can open up opportunities that simply aren’t there in stronger markets.

Periods like this can feel overwhelming, particularly when multiple financial pressures hit at once. But it’s important to step back. Markets have navigated global shocks before. The Savings and Loans crisis was one, the Oil Crisis in the 70’s another. Then we had a GFC which is when I started in this industry, then COVID, then Tarrifs and now another Oil crisis. There’s more. While the short-term can be uncomfortable during periods of uncertainty, the long-term fundamentals tend to hold for Australian property.

Australia continues to see strong population growth, a structural undersupply of housing, and a resilient and, what some economists call, a prudent financial system. Those drivers haven’t changed.

Final Thoughts

We won’t sugarcoat it; this is a challenging environment. No one really knows how things will unfold. Strategy is more important than ever, and what is really in your best interests must be considered. Is a fixed rate loan needed? Is a loan extension needed? Should a cash buffer be accessed or that approval be obtained before higher rates make servicing even tighter? While we need to understand what is happening now, we also need to keep an eye on what’s likely to happen in the long term based on what has happened in the past. There are many things still in our control during these times and as you’ve heard before, if you fail to plan, you plan to fail. If you’d like to talk through your situation, or simply understand what this means for you, reach out to our team and we’ll make sure your strategy is in your best interest.