2026 Budget Update: Our View After Digging Into The Details

Last updated: 24 May 2026

We’ve now had a few weeks to properly assess the Federal Budget changes and what they could mean for borrowers, investors and the broader property market.

We’ve put together a simplified visual breakdown of the proposed changes, how lenders are already responding, and the questions we’ve been asked most over the past few weeks.

While parts of the policy are still to be legislated, the implications for lending strategy and property decisions are already becoming clearer.

Key Takeaways

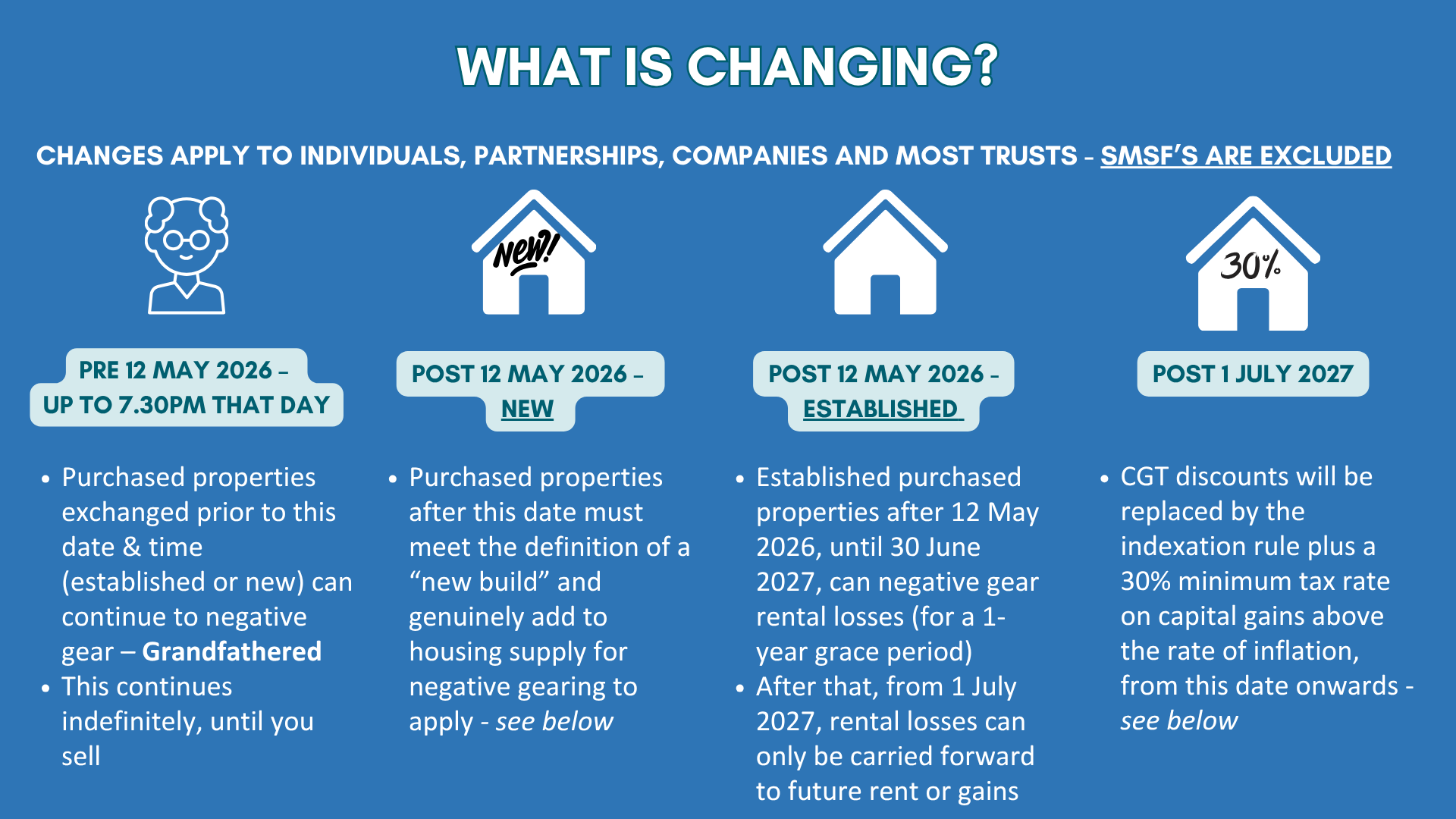

Existing investment properties purchased before 12 May 2026 remain grandfathered

New builds will continue to qualify for negative gearing

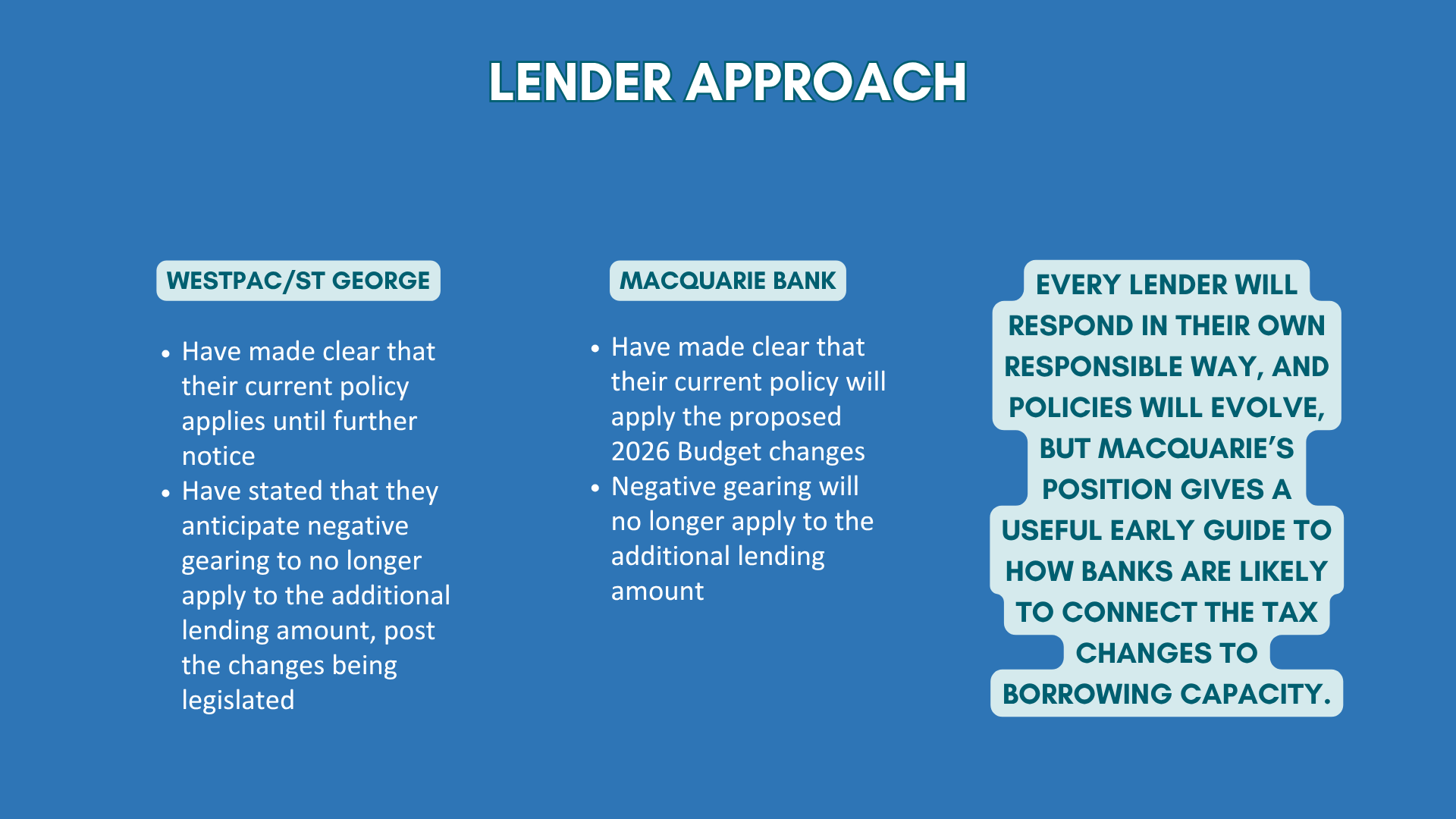

Some lenders have already begun adjusting servicing policy

Borrowing capacity for established investment properties may reduce

The reforms are designed to support first home buyers and new housing supply

Our Thoughts

More FHB’s than forecasted:

The playing field appears to be shifting more in favour of first home buyers and new housing supply, making it more appealing if looking to buy your first home. The government suggested that we will see an additional 75,000 first home owners over the next decade. If the Home Guarantee Scheme springboarded first home buyer loans 6.8 per cent to 31,783 in the December quarter 2025, according to the Australian Bureau of Statistics (ABS), we see 75,000 being hit easily. Well before the next decade is over.

The aspirational need to shift their strategy:

At the same time, the aspirational person looking at property as a means for wealth creation, especially the rent-vester, will need to reconsider their approach now. Those strategies that were put in place 3 months ago, or even a month before the budget, may need to be revisited. Preapprovals for investment properties in particular, need to be reviewed.

Fundamentals of property:

We’ve always focused on helping people make sound property decisions. We pay for and rely on objective data, we deploy a risk-based approach and use our experience to de-risk property purchases. We’re focused on good assets that have strong fundamentals, and with a view to the long term. Now, this will become even more of a focus for all people looking at property.

Investor-led markets:

Those investor-led markets will face pressures as more attention is drawn to quality stock. There is data available that allows you to see which suburbs are owner-occupier dominant, versus investor.

Serviceability hit:

Last week, we explored the detrimental serviceability impacts to investors buying established property without negative gearing. Macquarie is already applying these changes.

Rents to increase:

The Budget will add pressure to rents as some investors hold and refuse to sell because they can’t buy again with the same negative gearing benefits.

Homes to be upgraded:

We may see property owners focus on upgrading, renovating or adding bedrooms to their family homes as a means to creating wealth, where there are no capital gains tax consequences.

To start your finance journey hit the ‘start today’ button below.

The proposed changes are not yet legislated and details may evolve. Lending policy between banks may also differ as institutions interpret the reforms individually. We will stay close to these changes as they get closer to being legislated.

If you have property goals or are thinking about obtaining approval for your first or even your next property, we recommend speaking to our experienced team to ensure your strategy is in your best interests. Understanding borrowing capacity, lending strategy, and long-term implications will become more important than ever.

FAQ’s

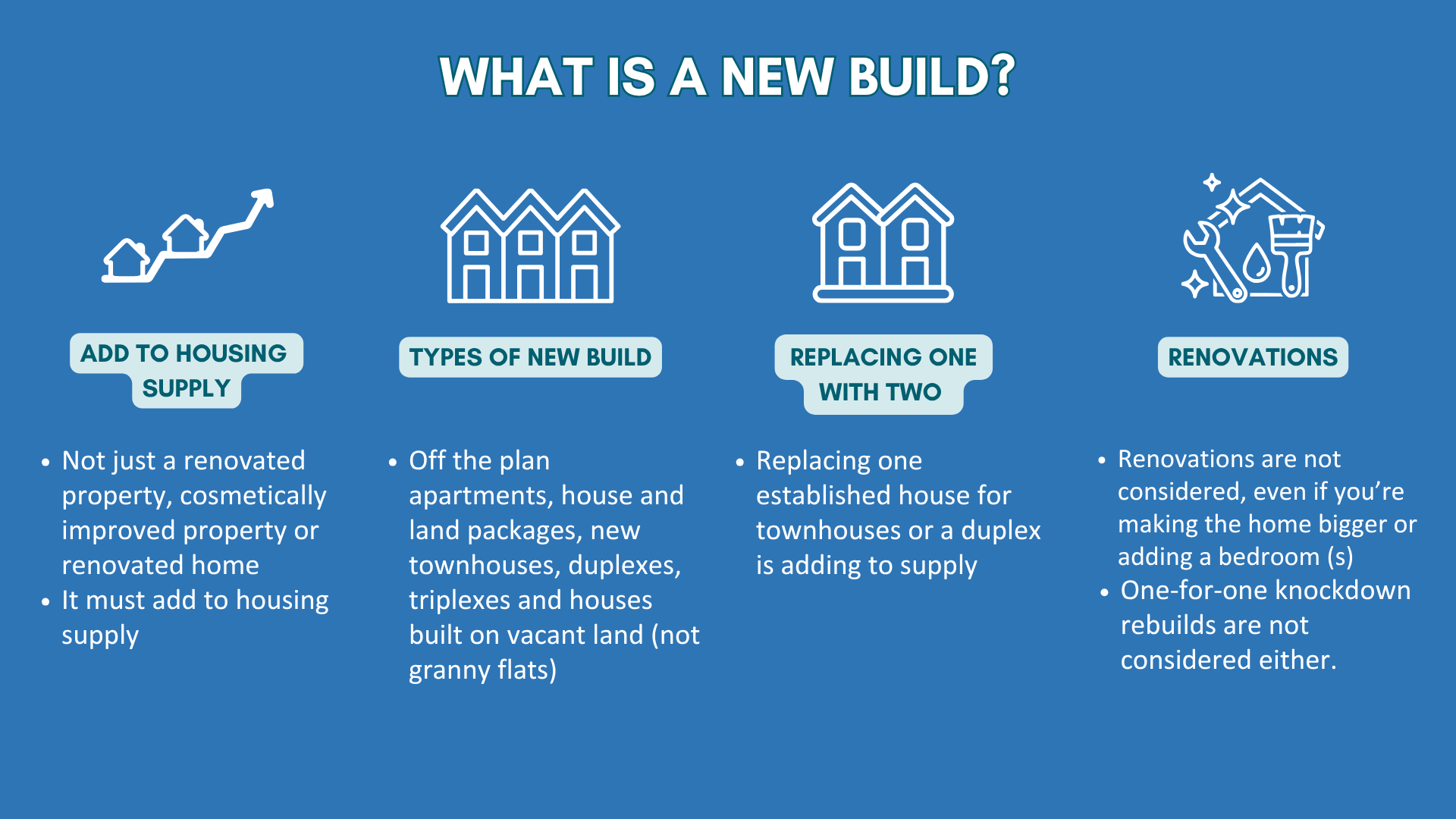

What is a 'new build' in Australia?

A newly constructed residential property that adds to housing supply. This may include a built house on vacant land, a new off-the-plan apartment, house and land package or a redevelopment of an existing property that creates more dwellings on that same parcel of land.

Can I negative gear my new build property?

Yes, new builds will allow investors to offset rental losses against taxable income such as wages or salary.

If I renovate my property, does that qualify as a new build?

No, if the improvements to a property do not add to housing supply, then the upgrade or renovation to the existing property, will not qualify as a new build. Substantial renovations do not fit the new-build definition.

How do the Capital Gains Tax (CGT) changes work?

For most assets held for longer than 12 months, the 50 per cent CGT discount is being replaced with two features: cost base indexation, which adjusts your cost base for inflation, and a 30 per cent minimum tax on capital gains accruing after 1 July 2027. See above for how the gain is calculated. Your accountant can work through your actual tax amount to pay, given the different tax rate bracket you may fall into.

Does this affect property held in my SMSF or in a managed fund?

SMSFs and widely held trusts, are excluded from the negative gearing changes entirely. These vehicles continue under existing rules, but you should still seek advice because super tax settings are complex and can change.

I already own an investment property. Am I affected?

If your investment property was under contract before 7:30pm, 12 May 2026, it’s grandfathered, meaning your existing negative gearing treatment can continue under current rules until you sell.

I’m thinking about buying an established investment property now. What changes?

For purchases between now and 30 June 2027, current negative gearing benefits can still apply, but from 1 July 2027 losses on established residential properties will not be negative geared but carried forward to future properties or to be used to offset gains from the sale of property.

Why are the banks changing the rules now if the changes are not yet legislated?

Because the Government has put clear dates and settings on the table, lenders treat the changes as a foreseeable shift that will affect a borrower’s ability to repay over the life of a 25–30‑year loan.

Responsible lending rules require them to factor these changes into servicing today, rather than assuming the 2025 tax rules will still apply in 2035 or 2040.

Need Help Understanding What This Means For You?

Whether you're purchasing your first home, reviewing an investment strategy, or reassessing borrowing capacity, our team can help you understand how these proposed changes may affect your plans.