2026 Budget: What It Means For Property

The 2026 Federal Budget has introduced some of the biggest property tax reforms Australia has ever seen.

Negative gearing for investors will be limited to new builds from 2027. Capital gains tax discounts will be reduced for future investment purchases.

The Government’s objective is clear: improve affordability for first home buyers and encourage more investment into new housing supply rather than established homes.

For many first-home buyers, this may finally create a fairer opportunity to compete in the market.

For investors, the changes alter borrowing capacity and investment strategy moving forward.

The lending impact

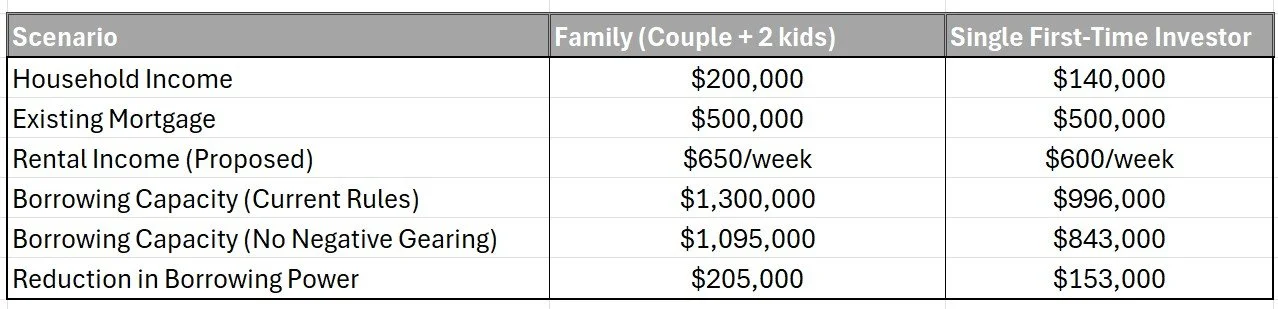

One of the immediate impacts will be on serviceability and borrowing power.

Historically, negative gearing has improved borrowing capacity for some investors because rental losses could be offset against personal income.

Without that benefit, the numbers can change quickly. Overnight, we modelled the below scenarios:

You can see that the reduction in borrowing power is quite significant.

For some investors, that may mean changing strategy, targeting different property types, or stepping away from certain markets altogether. At the same time, reduced investor competition should create greater opportunities for first-home buyers in established housing markets.

The Detail In Negative Gearing

Properties purchased before 12 May 2026, including those already under contract but not yet settled, will be grandfathered, meaning existing negative gearing arrangements can continue.

For properties purchased after 12 May 2026, current negative gearing benefits will remain available until 1 July 2027.

From that date onward, negative gearing for residential investment properties will only apply to newly built homes.

For investors purchasing established properties after 1 July 2027, rental losses will no longer be able to be offset against personal income, such as salary or wages. Instead, those losses will generally need to be carried forward and applied against future rental income or future capital gains.

Capital Gains Tax Discount

The Government has also announced significant changes to capital gains tax arrangements.

The current 50% capital gains tax discount for assets held longer than 12 months will be removed from 1 July 2027 and replaced with:

a new inflation-adjusted cost base system, and

a minimum 30% tax rate on net capital gains.

Importantly, these changes apply not just to property but across multiple asset classes.

Assets acquired before 1985 and sold prior to 1 July 2027 will remain exempt from capital gains tax. However, assets sold after that date may become subject to the new framework.

Will this solve affordability?

Perhaps partially is our view at Black and White Finance. Australia’s housing affordability challenges have never been driven by one issue alone.

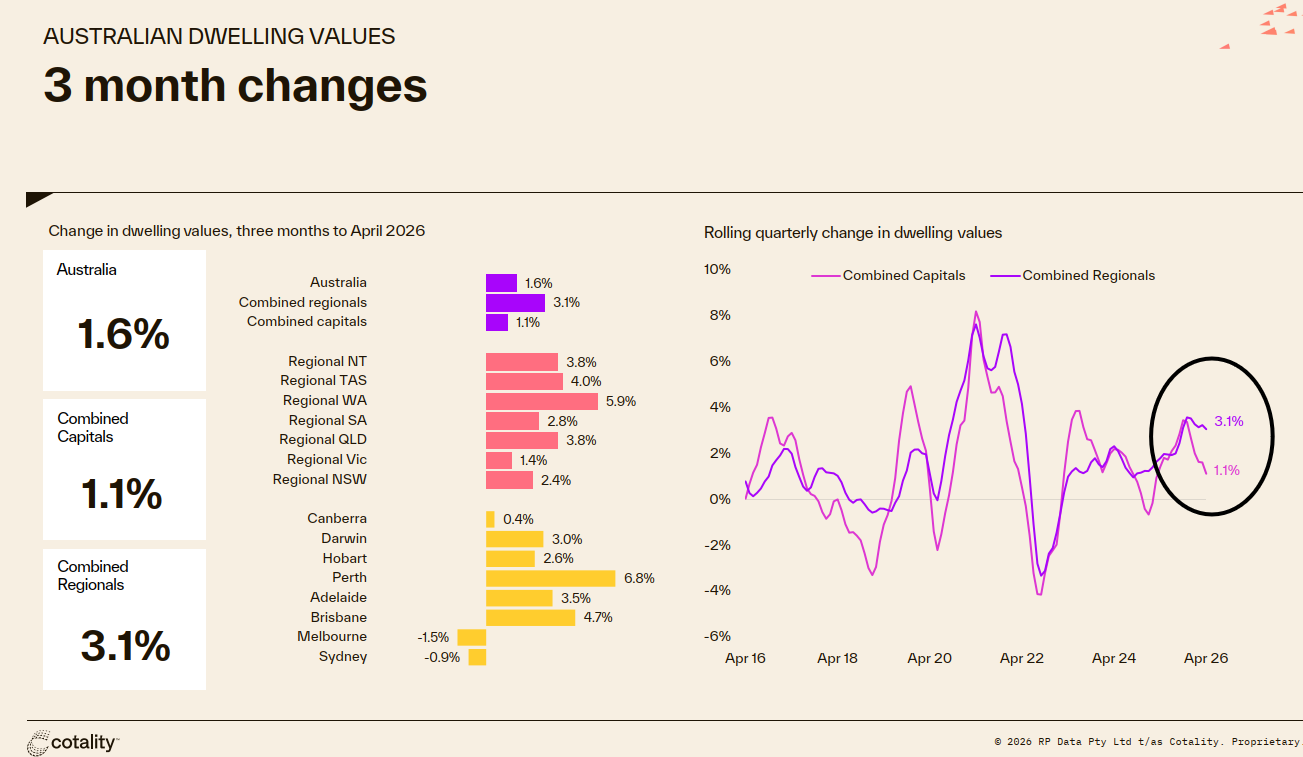

Higher interest rates, population growth, construction costs, planning delays, limited housing supply, and tighter lending conditions have all contributed to the pressures borrowers face today. You can see that in rolling quarter change in dwelling values above from Cotality which shows that growth is slowing.

Cotality Monthly Housing chart for May 2026

The Government hopes these reforms will help approximately 75,000 additional first home buyers enter the market over the next decade.

At the same time, the broader issue of housing supply remains.

While some investors may now sit on the sidelines and allow first home buyers a fairer opportunity, Australia still needs significantly more housing stock built over the coming years to support long-term demand.

Property markets remain resilient, long-term

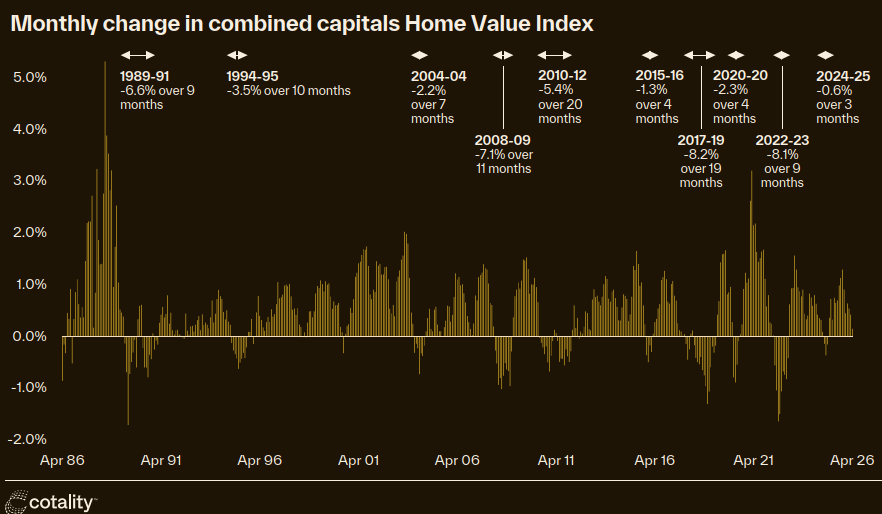

The broader property market is already softening under the weight of higher interest rates and affordability pressures. As you can see above.

But property markets have always moved in cycles.

Australia has navigated major disruptions before, including the GFC, pandemic, inflation shocks, rising interest rates, and global uncertainty. See below from Cotality, from the same monthly housing chart referred to above. You can see the up's and down's.

And despite those challenges, property has continued to demonstrate long-term resilience, largely because the underlying fundamentals of housing supply and population growth remain.

According to Cotality, most housing downturns over the past 40 years have lasted less than 12 months.

Final thoughts

Our government hopes that these changes will create a fairer go for first home buyers, and investors will be forced to alter their strategies. When you put your head down, work your backside off, and save, you should be able to buy your own home and this budget seems to support that aspiration. Time will tell how it all unfolds.

Moving forward, the focus for perhaps the investor on the other hand may shift toward:

new builds

stronger cash flow and rental yield

more sustainable lending structures

people putting more money into their own family homes to create wealth

less of a focus on purely tax-driven investing

And for borrowers generally, understanding borrowing capacity, lending strategy, and long-term affordability will become more important than ever.

If you’d like to walk through how this affects your purchase plans or your current loan, reach out to the Black and White Finance team.

To start your finance journey hit the ‘start today’ button below.