Election 2025: Property promises — Opportunities or Risks?

With the federal election set for 3rd May 2025, both Labor and Liberal parties are unveiling major property-related promises, particularly aimed at first home buyers. At first glance, the policies sound positive. But a closer look reveals broader risks that could reshape the market far beyond the short-term. While these initiatives might help some buyers into the market, they also risk driving house prices even higher, saddling new homeowners with bigger debts, and shifting more financial risk onto taxpayers. The impacts could last well beyond this election cycle.

Labor's Plan: Expanding the First Home Guarantee Scheme

Labor is promising to expand the current First Home Guarantee Scheme, helping buyers get into a home with just a 5 per cent deposit, without paying Lenders Mortgage Insurance (LMI).

Generally, when purchasing a home, a 20 per cent deposit is ideal – if the deposit is less than 20 per cent, typically an LMI premium is paid, and a higher interest rate is applicable.

Under this scheme, first-time owners can purchase or build a home with as little as a 5 per cent deposit, avoid paying LMI, and get access to a cheaper interest rate.

While this could open doors for many, it also comes with serious risks:

• It effectively nationalises a large chunk of the mortgage insurance market, putting taxpayers on the hook for defaults (the number of defaults is expected to be low but it is nonetheless a risk).

• Smaller banks could be squeezed out by the Big Four, hurting competition for future borrowers.

• Encouraging low-deposit loans, encourages higher mortgages which increases the risk that borrowers could fall into negative equity if prices dip because they are borrowing 95 per cent of a property's value.

This Home Guarantee expansion is part of the $43 billion Homes for Australia plan.

Labor is also promising to deliver:

100,000 homes for first home buyers, by investing $10 billion to support infrastructure, land purchases and construction.

A Help to Buy shared equity scheme offering up to 30 per cent equity for existing homes and 40 per cent for new builds, with buyers needing just a 2 per cent deposit.

Prefab and modular homes, which can be used to speed up the building time in comparison to traditional homes, will receive $54 million.

$120 million towards incentivising states to remove red tape and streamline building approvals

$78 million towards fast tracking the qualification of 6,000 tradies

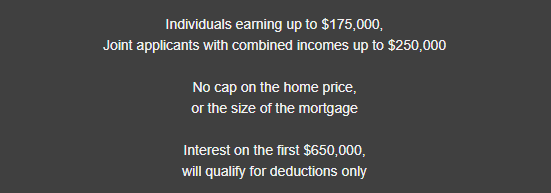

Liberals' Plan: Mortgage Interest Deductions

The Liberal Party is offering a tax deduction for interest paid on the mortgage for a first home buyer. Interest paid on the first $650,000 of a loan on new homes, for the first five years, would be deductible.

This Liberal Party Affordable Housing promise sounds generous, but experts are warning of the risks:

• It will be tricky for banks to then factor this negative gearing into future serviceability assessments.

• It favours higher-income earners, who benefit more from tax breaks, raising questions about fairness.

• It also encourages bigger mortgages and higher leverage, leaving borrowers more exposed to negative equity, similar to Labor's initiative.

• There’s a risk of borrowers manipulating incomes (those self-employed more so) to qualify.

• After the five years are up, once the negative gearing benefit drops off, many borrowers will face a jump in costs to their household as they'll need to pay more tax, creating political pressure for further extensions.

The Liberal Party is also promising:

A 2-year ban on foreign investors and temporary residents purchasing existing homes, to ease demand.

Reducing migration levels and the number of foreign students at universities, and also increasing student visa fees.

Investing in essential infrastructure like water, power, sewerage and roads at housing development sites, which should unlock up to 500,000 new homes.

Provide new incentives to small and medium businesses to hire and train apprentices, with a target of 400,000 new tradies to be added to the workforce.

A 10 year freeze on any changes to the National Construction Code.

The Bigger Issue: Housing Supply is Still the Bottleneck

Both Labor and Liberal policies will boost buyer demand, that's for sure.

When national house prices are already rising sharply, with Adelaide now joining the $1 million median price club, and Sydney's median is up around $1.7 million, adding more buyers, without increasing housing supply, could fan the flames even further.

See here from Domain's March 2025 House Price Report:

As it stands:

Construction costs for materials are high.

State planning and zoning rules are slow and complex.

There’s a critical shortage of skilled tradespeople.

Stamp duty and GST expenses, when added to high build costs, are detrimental to profits for developers.

Labor is pledging 100,000 new homes for first home buyers through a $10 billion fund, the Coalition says their new home tax break will boost supply indirectly, by encouraging new builds.

Most economists agree, however, that without faster approvals, more density, lower costs or incentives for developers, and better productivity in construction, housing supply won't keep up.

AMP's economist Shane Oliver sees house prices rising in 2025 by around 3 per cent, with lower rates and more generous measures for first home buyers, regardless of who wins the election, being promised to the market.

Final thoughts

The 2025 election is bringing big property promises, for first home buyers especially, but not without controversy. Both Labor and Liberal are offering major incentives in an attempt to support supply, but will most likely further boost buyer demand. With the supply of new properties tight and the time it ultimately will take for these initiatives from either party to kick in, higher prices, bigger mortgages, and taxpayer exposure could all be on the cards this year and into the future.

As the election unfolds, the government and banking policies change, and the economy continues to shift this year, staying informed is more important than ever. Whether you're reassessing your loan structure, planning a purchase, or just want to explore your options, we’re here to guide you every step of the way.

If you want to know more about different rates, terms, or bank specials currently available, please send a note to info@blackandwhitefinance.com.au, or click the start today button a little lower.

Reach out to us on

0448 890 186

or

Send us a quick online enquiry by clicking the START TODAY button

Feedback

We’d love to hear what you think about our content or how we could improve to make your experience better. Please send a note to peter@blackandwhitefinance.com.au to let us know your thoughts.

If you'd like to help keep family or friends in the know or let us help them, we’d be more than happy for you to share this blog using the links here.